The Real Estate Production Company DBA Agenta ("Agenta," "we," "us," "our") provides websites, hosting, digital marketing and other technology to our clients ("Clients") in the real estate industry. Our services help real estate professionals enhance their online presence and manage their digital marketing efforts

This Privacy Policy describes how we collect, use, and protect personal information when you visit the websites of our Clients. As a visitor to our Clients' websites ("Sites"), this policy applies to you. Our Clients' branding may be displayed on the Site you are interacting with, but Agenta is responsible for providing the underlying technology and services.

If you are a visitor to one of our Clients' Sites, this Privacy Policy applies to you and describes Agenta's policies and practices regarding the collection, use, and disclosure of your personal information. Agenta provides these services solely as a service provider and data processor, using the personal information collected at the direction of our Clients.

This Privacy Policy does not apply to any websites, applications, or other online services that do not link to this policy, including other services provided by our Clients. Please contact the Client directly to learn about how they use your personal information.

1. Information We Collect

1.1. Information You Provide to Us

- Contact Information: We collect contact information that you provide, such as your name, email address, and phone number.

- Payment Information: For transactions, we collect payment details, but this information is tokenized and processed securely by our payment provider.

- Communications: When you contact us for support or provide feedback, we collect your correspondence.

- Other Information: We collect other information not listed here that you may provide to us voluntarily in connection with your interactions with the Client through the Site or Services.

1.2. Information We Collect Automatically

- Usage Information: We collect details about your interactions with our Services, such as IP address, browser type, pages viewed, and the time spent on our site.

- Cookies and Similar Technologies: We use cookies to remember your preferences and track your activity on our site. For more details, see our Cookie Policy.

1.3. Information from Third Parties

- Social Media Information: If you interact with us on social media platforms, we may receive information from those platforms according to their privacy policies.

- Other Sources: We may receive information about you from other third parties, such as marketing partners, public databases, or data providers.

2. How We Use Your Information

We use your information to:

- Provide, operate, and improve our Services.

- Personalize your experience and deliver content relevant to your interests.

- Improve our website and Services through data analysis and research.

- Provide support, and respond to requests, questions, and feedback.

- Provide marketing and advertising Services on behalf of our Clients.

- Ensure the security and integrity of our Services.

- Comply with legal obligations and resolve disputes.

- Send marketing communications, in compliance with the CAN-SPAM Act.

3. How We Share Your Information

We do not sell or share your personal information with third parties for marketing or promotional purposes. We may share your information with:

- Service Providers: Companies that help us operate our business, such as hosting services, payment processors, and analytics providers, who are required to keep your information confidential.

- Legal Requirements: When required by law, such as to comply with a subpoena or similar legal process.

- Business Transfers: In the event of a merger, acquisition, or sale of all or a portion of our assets, your information may be transferred to the new owner.

4. Your Rights Under CCPA

Under the California Consumer Privacy Act (CCPA), California residents have the right to:

- Know: Request information about the personal data we collect, use, and share about you over the past 12 months.

- Access: Obtain a copy of your personal data.

- Delete: Request the deletion of your personal data, subject to certain exceptions.

- Opt-Out: Decline the sale of your personal data, though we do not sell personal data.

- Non-Discrimination: Not be discriminated against for exercising any of your CCPA rights.

To exercise these rights, please contact us at ccpa@agentawebsites.com. We will respond to your request within 45 days.

5. Data Retention

We retain your information as long as necessary to provide our Services and comply with legal obligations. If you request deletion of your data, we will remove it unless we are compelled to retain it for legal reasons.

6. Data Security

We use various security measures to protect your personal information. These include encryption, access controls, and regular security assessments. While we strive to ensure the security of your data, no method of transmission over the Internet or electronic storage is 100% secure.

7. Cookies and Tracking Technologies

We use cookies to enhance your experience on our site. You can manage your cookie preferences through your browser settings. Disabling cookies may affect the functionality of our Services. For more information, please see our Cookie Policy.

8. Do Not Track

We honor Do Not Track (DNT) signals and do not track, plant cookies, or use advertising when a DNT browser mechanism is in place.

9. Third-Party Services

Our site may contain links to third-party websites and services. We are not responsible for the privacy practices or content of these third-party sites. Please review their privacy policies to understand how they collect and use your information.

We use third-party services such as Google Analytics, Google Ads, and Meta Ads (formerly Facebook Ads) to:

- Understand and improve the performance of our Services.

- Remarket advertising to you on behalf of our Clients.

These services may collect information about your use of our website, including your IP address, browser type, and browsing activities. The data collected by these third parties is used to provide insights into website traffic, user behavior, and marketing effectiveness.

You can learn more about how these third-party services use your data and opt-out of their data collection by visiting their respective privacy policies:

10. Text Messaging and FTC Compliance

We adhere to FTC requirements regarding text messaging to protect you from unwanted and unlawful texts. This includes blocking texts from illegitimate numbers and providing a point of contact for reporting any issues. For more details on these requirements, please visit the FCC's website.

11. International Data Transfers

Although we do not currently transfer data internationally, we will ensure that any future international data transfers comply with applicable laws and regulations to protect your data.

12. User Rights and Control

In addition to CCPA rights, you may have the right to access, correct, or delete your personal information, object to or restrict processing of your data, and request data portability. Please contact us at legal@agentawebsites.com to exercise these rights.

13. Incident Response

In the event of a data breach, we will notify affected users within 72 hours of becoming aware of the breach, as required by applicable laws. We will take immediate steps to mitigate the breach and prevent future incidents.

14. Data Minimization and Accuracy

We are committed to collecting only the personal data that is necessary for the purposes outlined in this policy. We take reasonable steps to ensure the accuracy and completeness of your personal information.

15. Children's Privacy

Our Services are not intended for use by children under 13, and we do not knowingly collect personal information from children under 13. If we learn that we have collected personal information from a child under 13, we will delete it.

16. Email Communications and CAN-SPAM Act

We comply with the CAN-SPAM Act. You can opt-out of receiving our marketing emails by following the instructions at the bottom of each email or by contacting us at optout@agentawebsites.com. We will promptly honor your request to be removed from our email lists.

17. Changes to This Privacy Policy

We may update this Privacy Policy from time to time. We will notify you of any changes by posting the new Privacy Policy on our website and updating the effective date. It is your responsibility to review this Privacy Policy periodically.

18. Contact Us

If you have any questions about this Privacy Policy, please contact us at:

Real Estate Production Company DBA Agenta

PO 22582

901 Broadway

Nashville, TN 37202

legal@agentawebsites.com

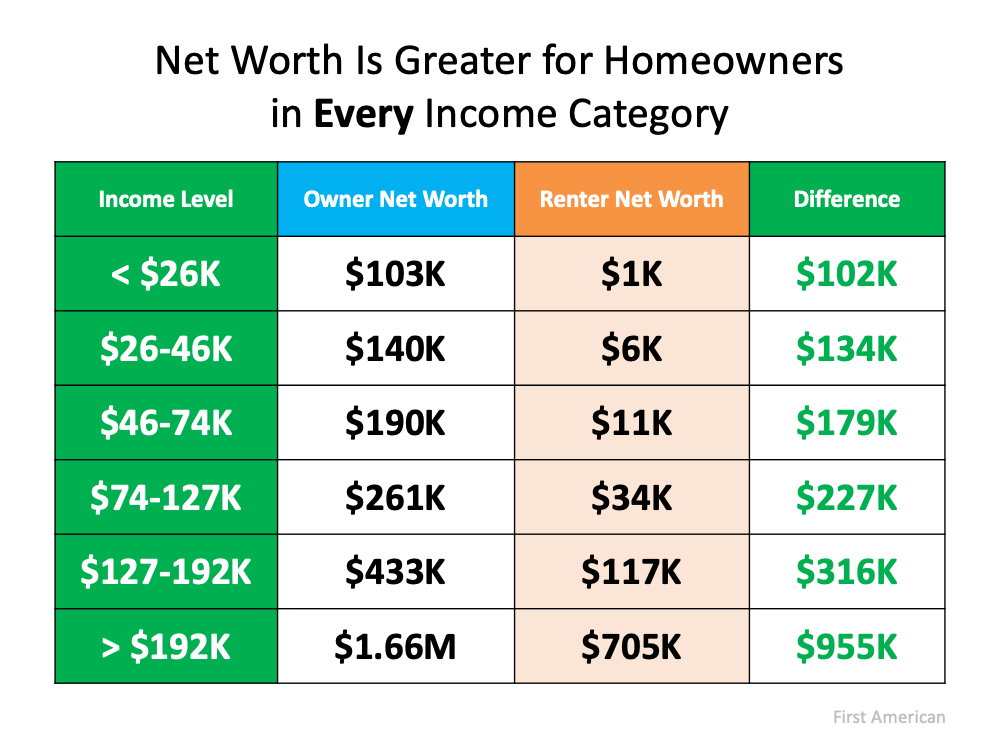

Owning a home is an essential steppingstone to grow a household’s net worth. Despite the slightly greater sacrifice in the percentage of monthly income you’ll spend on housing today, for most homebuyers, the payoff of starting to build equity now will be worth it.

Owning a home is an essential steppingstone to grow a household’s net worth. Despite the slightly greater sacrifice in the percentage of monthly income you’ll spend on housing today, for most homebuyers, the payoff of starting to build equity now will be worth it.